The way people manage payments has changed quickly in recent years. Traditional cards made of plastic are no longer the only option for accessing credit. Today, many banks and financial institutions are offering digital credit cards designed to simplify transactions and improve security.

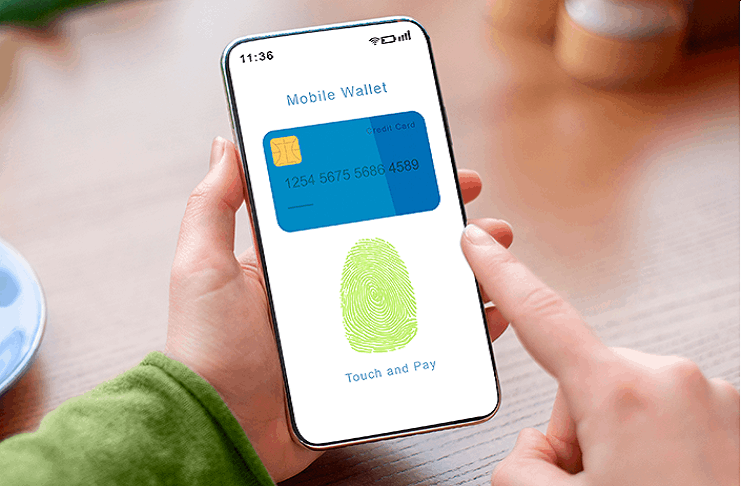

A digital card works entirely online, without the need for a physical version. It can be stored in your smartphone, used for online shopping, and linked to digital wallets. This type of card is becoming popular among those who want fast approval processes, better control of expenses, and additional protection against fraud.

Understanding how a light digital credit card works is essential if you are looking for flexibility in your personal finances. It combines the basic functions of a traditional credit card with the advantages of digital technology. Below, we’ll explore what makes these cards different, how they operate, their main benefits, and what you should consider before choosing one.

Fuente Imagen: Resuelve tu deuda

Defining a Digital Credit Card

A digital credit card is an electronic version of a traditional credit card. Instead of receiving a plastic card, the user is given digital credentials that can be stored in mobile wallets such as Apple Pay or Google Wallet. These credentials include the card number, expiration date, and security code, all available through the bank’s app.

The concept of a “light” card refers to the fact that it is faster to issue, requires fewer procedures, and in many cases does not involve annual fees. Financial institutions promote them as a more efficient and eco-friendly alternative, since there is no physical material involved.

Unlike prepaid cards or debit cards, a digital credit card still gives you access to a credit line. This means you can buy products, pay for services, and spread payments over time, exactly like with a traditional credit card. The difference lies in its format and the way it integrates into your digital lifestyle.

How Does a Digital Credit Card Work?

When you apply for a digital credit card, the issuing bank approves the line of credit and immediately generates the digital details. Instead of waiting for a physical delivery, you can use the card as soon as the approval is confirmed. This allows instant access to purchases, subscriptions, and online services.

Payments are processed in the same way as with a standard card. The only difference is that the card details exist virtually, and you use them through a phone, computer, or smartwatch. Many users prefer adding the card to a digital wallet so they can pay by tapping their device on contactless terminals.

Monthly billing cycles, interest rates, and repayment methods remain the same. You still receive a statement from the bank, which shows your purchases, minimum payment, and total balance. In this sense, it works exactly like a plastic card but in a more flexible format.

Fuente Imagen: Reporte Indigo

Advantages of Using a Digital Credit Card

Faster Access

One of the biggest advantages is the speed of issuance. With traditional credit cards, you may wait several days for delivery. A digital card is activated almost instantly after approval, meaning you can shop or subscribe to online services without delay.

Greater Security

Digital credit cards often come with advanced security features. Many allow temporary card numbers that expire after a single purchase, reducing the risk of fraud. Biometric authentication, such as fingerprint or facial recognition, adds another layer of protection when making payments.

Convenience for Online Shopping

Because the card is designed for digital use, it is ideal for e-commerce, app subscriptions, and online services. The user does not need to carry a physical card, which makes the process lighter and more convenient.

Lower Costs

Some institutions market these cards as “light” because they reduce or eliminate annual fees. With fewer administrative and material expenses, banks can provide more affordable services to their customers.

Comparing Digital and Traditional Credit Cards

Traditional credit cards remain popular for in-person payments, especially for those who prefer carrying a physical card. However, they are less efficient for people who mainly shop online.

Digital credit cards are better integrated into modern payment systems. They work smoothly with mobile wallets, subscription services, and online platforms. They also offer faster setup, which is attractive for younger users and those who prioritize immediacy.

From a security perspective, digital cards usually outperform physical ones. Features like dynamic CVVs (security codes that change frequently) reduce exposure to fraud. On the other hand, traditional cards are still necessary in some contexts, such as countries or businesses that do not yet accept digital wallets.

Who Should Consider a Digital Credit Card?

A digital credit card is best suited for people who rely heavily on online transactions. If you often buy from e-commerce stores, pay for streaming services, or make in-app purchases, this type of card can simplify your routine.

It is also ideal for individuals who value security. Features like biometric verification and virtual numbers provide peace of mind. Additionally, people who want to avoid physical clutter or prefer eco-friendly financial solutions may also find digital cards appealing.

On the other hand, if you frequently travel to places where contactless payments are not available, you might still need a physical backup card. Evaluating your lifestyle is the best way to decide whether a digital or traditional credit card is more practical.

Fuente Imagen: Scotiabank Colpatria

Potential Limitations to Keep in Mind

While digital credit cards offer many benefits, they are not perfect. Some users may face acceptance issues in certain stores that do not support digital payments. Also, not every financial institution offers the same conditions, so fees and benefits vary widely.

Another point to consider is technology dependency. You need a smartphone or digital device to make payments, which can be a disadvantage if your phone runs out of battery or is lost. Although backup methods exist, reliance on technology can still create inconveniences.

Lastly, users must remain disciplined with spending. The speed and convenience of digital payments can encourage overspending if budgets are not carefully monitored.

-

Practical Examples of Use

Imagine you are subscribed to multiple digital platforms such as music, movies, and gaming services. A digital credit card makes it easier to manage these subscriptions without carrying or exposing a physical card number.

Another example is when shopping on foreign websites. Some digital cards provide better exchange rate protection and issue disposable card numbers, which makes international transactions safer.

For frequent travelers, having a digital card means you can make hotel reservations, buy plane tickets, and pay for services abroad with fewer risks of card cloning. These real-world cases highlight how digital cards are adapting to modern consumer needs.

FAQs About Digital Credit Cards

Do I Need a Physical Card With It?

No, the idea of a digital card is to operate entirely without plastic. However, some banks offer an optional physical version in case you need it for specific situations.

Is It Safe to Use a Digital Credit Card?

Yes, most come with advanced features like biometric logins and disposable card numbers. Security depends on how you manage your device and personal data.

Can I Use It in Stores?

Yes, but only in stores that accept contactless payments through digital wallets. Otherwise, you may need to input card details manually.

Are Fees Lower Than Regular Cards?

In many cases, yes. Some banks waive annual fees or lower them because the card is “light” in terms of cost and maintenance.

Conclusion

Digital credit cards represent a natural step in the evolution of payment systems. They combine the flexibility of traditional credit with the efficiency of digital tools. For users who shop online frequently, they provide instant access, greater security, and lower costs.

At the same time, limitations such as acceptance in certain stores and reliance on devices should be carefully considered. Choosing a digital card depends on your lifestyle, spending habits, and the services offered by your bank. By analyzing these factors, you can decide whether adopting a light digital credit card is the right move for your financial routine.